With a market capitalization of $50.6 billion, Targa Resources Corp. (TRGP) is a leading midstream energy infrastructure company focused on the gathering, processing, transportation, and export of natural gas and natural gas liquids (NGLs). Headquartered in Houston, Texas, Targa plays a critical role in connecting upstream production with downstream markets, particularly in key shale basins, like the Permian Basin.

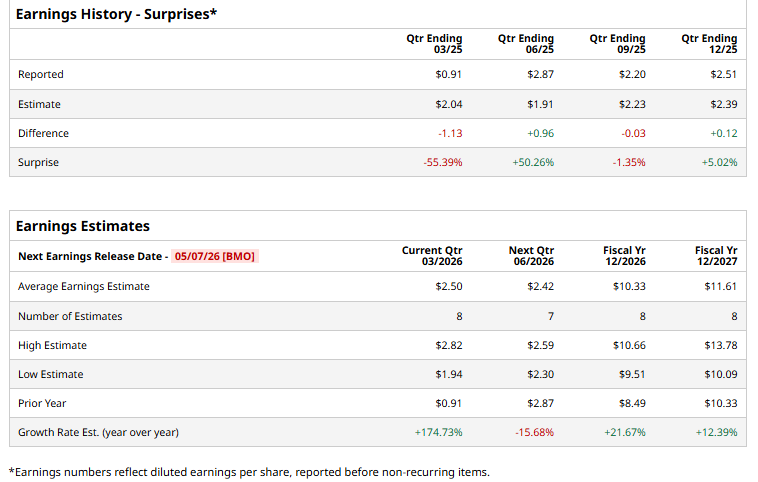

The energy titan is expected to release its Q1 2026 earnings on Thursday, May 7, before the market opens. Ahead of the event, analysts expect the company to generate a profit of $2.50 per share on a diluted basis, up 174.7% from $0.91 per share in the year-ago quarter. The company has surpassed Wall Street’s EPS estimates in two of its last four quarters, while missing on two other occasions.

For the current year, analysts project the company’s EPS to be $10.33, up 21.7% from $8.49 in fiscal 2025. Moreover, its EPS is expected to rise 12.4% year over year to $11.61 in fiscal 2027.

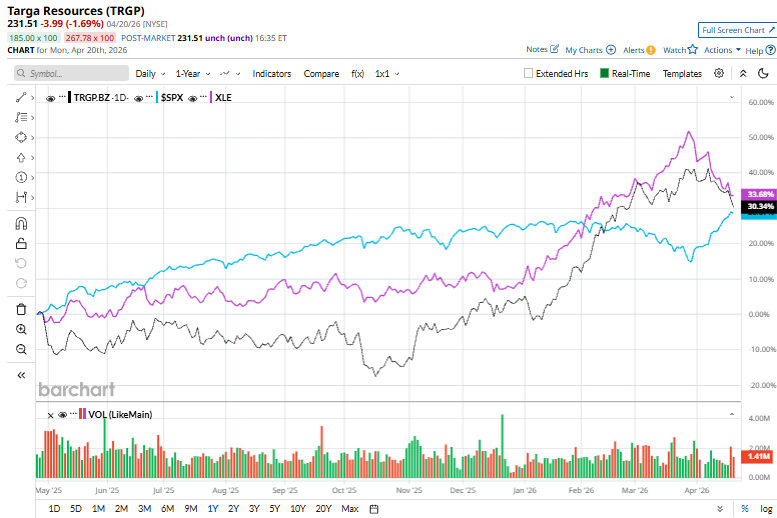

Shares of Targa Resources have surged 32.6% over the past 52 weeks, underperforming the S&P 500 Index’s ($SPX) 34.6% rise and the State Street Energy Select Sector SPDR ETF’s (XLE) 35.1% return during the same time frame.

Targa Resources shares rose marginally after the company approved a 25% increase in its quarterly cash dividend, raising it to $1.25 per share, or $5 on an annualized basis, for the first quarter of 2026. This increase aligns with the company’s previously communicated capital return strategy and reflects confidence in its cash flow generation and operational outlook.

The dividend will be paid on May 15, 2026, to shareholders of record as of the close of business on April 30, 2026. The higher payout marks a significant step-up from the dividend declared in the same period last year, signaling Targa’s continued focus on returning capital to shareholders while benefiting from strong volumes and demand across its midstream energy operations.

Analysts are highly bullish on TRGP, with the stock having a “Strong Buy” rating overall. Among the 22 analysts covering the stock, 18 are recommending a “Strong Buy,” one recommends a “Moderate Buy,” and the remaining three analysts suggest a “Hold” for the stock. TRGP’s average analyst price target is $207.91, indicating an upside of 12.2% from the current levels.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Raymond James Is Betting Okta Stock Can Gain from Here. Should You Buy Shares Now?

- Massive and Unusual Trading in Home Depot Call Options - Is the HD Stock Rally Over?

- Will Q1 Earnings Power GE Vernova Stock to $1,225?

- PayPal Stock Is Down More Than 80% Over the Past 5 Years. Michael Burry Is Buying the Dip.